Your 2026 Planning Roadmap

The 2026 financial landscape is all about saving smarter. New IRS rules are reshaping how high earners, retirees, and business owners should think about taxes, retirement, and education funding. If your plan hasn’t been updated, you may be leaving meaningful opportunities on the table.

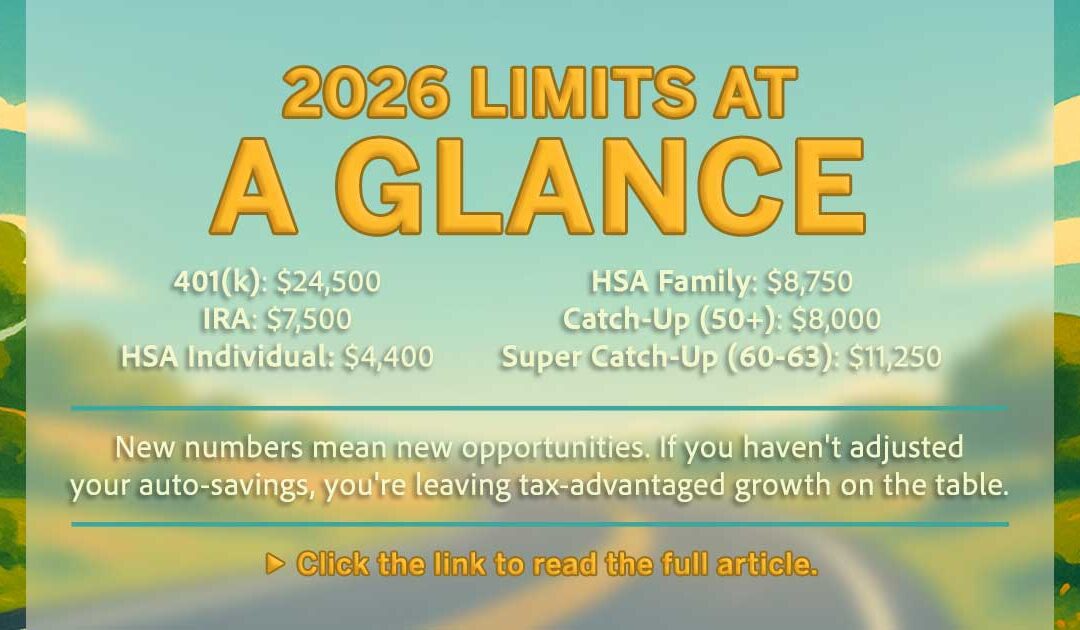

Below are the key changes that matter most.

Higher Contribution Limits

- 401(k), 403(b), employer plans: $24,500

- IRAs (Traditional + Roth): $7,500

- HSAs: $4,400 (individual) | $8,750 (family)

Catch-Up Contributions

- Age 50+: Standard catch-up contributions increased to $8000.

- Ages 60–63: As of 2025, a new Super Catch-Up rule increases the standard catch-up contribution to $11,250 in additional employer-plan contributions, but only during this narrow age window.

Mandatory Roth Catch-Up for High Earners

If your 2025 wages exceeded $150,000, all 2026 catch-up contributions to workplace plans must be Roth.

- Taxes are paid today, but future growth and withdrawals are tax-free.

- If your plan doesn’t offer a Roth, you may be unable to make catch-up contributions until it does.

Planning Strategies to Help Control Taxable Income

- Professionals: Maximize pre-tax retirement and HSA contributions to reduce AGI.

- Retirees: Use Qualified Charitable Distributions (QCDs) and donor-advised funds to manage taxes and RMDs.

- Business Owners: New retirement plans may qualify for 100% startup tax credits (up to $5,000/year for 3 years) and employer contribution credits of up to $1,000 per employee.

529 Plans: More Flexible Than Ever

- Up to $20,000 per year, per child for private K–12 tuition.

- Funds may now cover tutoring, test prep, and certain therapies.

- State tax treatment may differ from federal rules.

The Bottom Line

These changes reward coordination, not guesswork. Whether you’re building your wealth, transitioning to retirement, or planning for the next generation, 2026 creates new opportunities, but only if you take an intentional approach with your strategy.

If you would like to understand how these changes impact your plan, contact us to schedule a brief review, so you’re positioned for the year ahead.

Disclaimer: The content provided herein is based on our interpretation of the new tax laws and is not intended to be legal advice or provide a tax opinion.